All Categories

Featured

Table of Contents

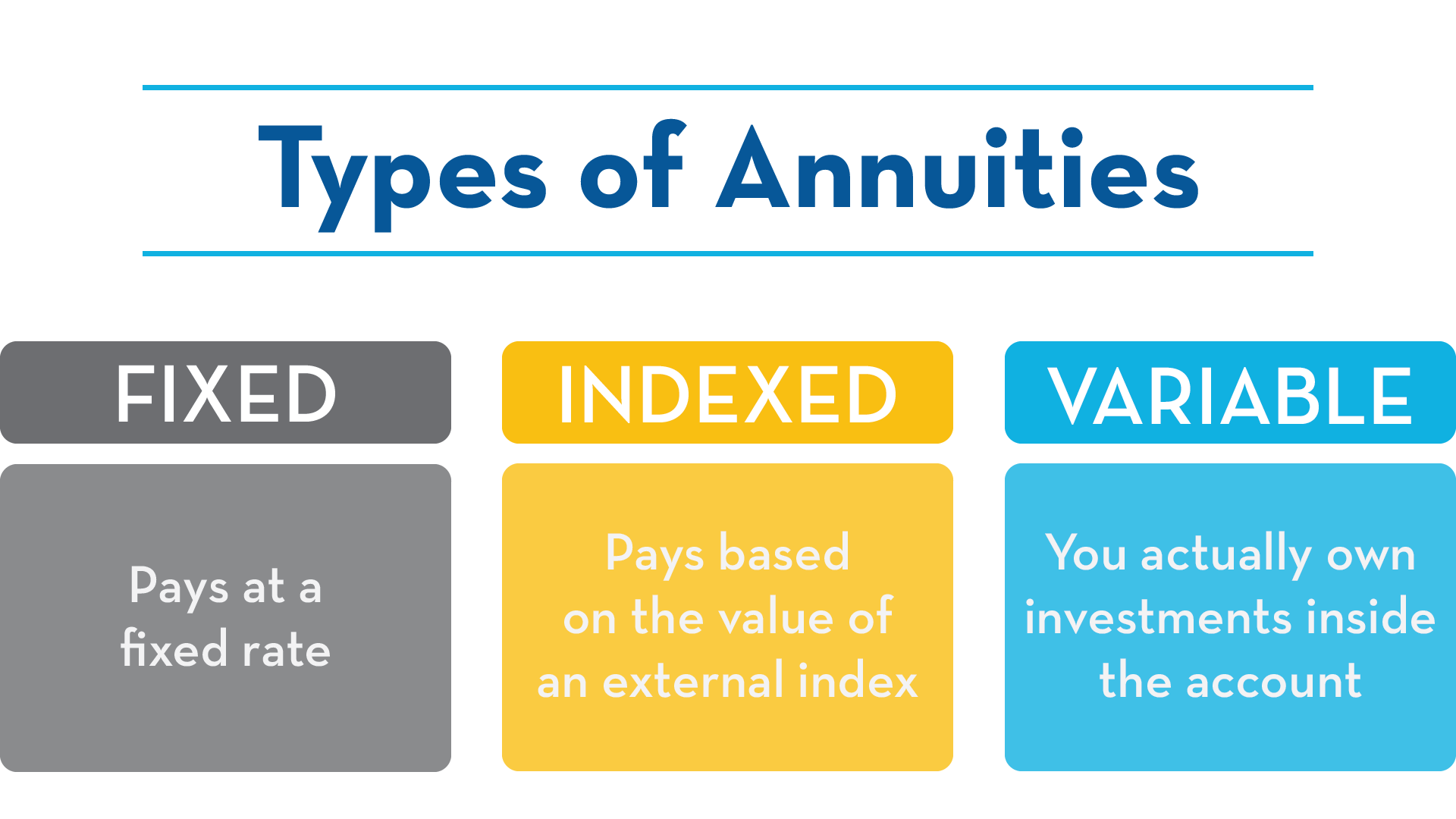

With a variable annuity, the insurance firm purchases a profile of shared funds selected by the customer. The efficiency of those funds will determine exactly how the account expands and how huge a payout the customer will ultimately obtain. People who choose variable annuities are eager to handle some degree of danger in the hope of creating larger revenues.

If an annuity buyer is wed, they can select an annuity that will certainly remain to pay earnings to their partner must they die initially. Annuities' payouts can be either prompt or delayed. The fundamental question you need to think about is whether you desire routine revenue currently or at some future day.

A credit enables the cash in the account even more time to expand. And much like a 401(k) or an individual retired life account (INDIVIDUAL RETIREMENT ACCOUNT), the annuity remains to gather incomes tax-free till the money is withdrawn. Gradually, that could construct up into a substantial amount and result in bigger settlements.

There are some various other crucial decisions to make in acquiring an annuity, depending on your conditions. These consist of the following: Purchasers can arrange for repayments for 10 or 15 years, or for the rest of their life.

Understanding Fixed Vs Variable Annuity Pros Cons Key Insights on Your Financial Future Breaking Down the Basics of Tax Benefits Of Fixed Vs Variable Annuities Benefits of Pros And Cons Of Fixed Annuity And Variable Annuity Why Fixed Vs Variable Annuity Matters for Retirement Planning Immediate Fixed Annuity Vs Variable Annuity: Explained in Detail Key Differences Between Pros And Cons Of Fixed Annuity And Variable Annuity Understanding the Key Features of Fixed Income Annuity Vs Variable Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Annuities Fixed Vs Variable A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

That might make good sense, for example, if you need an income increase while settling the last years of your home mortgage. If you're wed, you can select an annuity that pays for the remainder of your life or for the rest of your spouse's life, whichever is longer. The last is often referred to as a joint and survivor annuity.

The choice in between deferred and instant annuity payments depends mostly on one's financial savings and future incomes objectives. Immediate payouts can be valuable if you are already retired and you need a resource of earnings to cover daily expenses. Immediate payouts can start as quickly as one month into the acquisition of an annuity.

People typically acquire annuities to have a retired life earnings or to construct financial savings for another function. You can get an annuity from a qualified life insurance agent, insurer, economic organizer, or broker. You must speak with an economic advisor about your demands and goals before you acquire an annuity.

The distinction between the 2 is when annuity settlements begin. You don't have to pay taxes on your earnings, or contributions if your annuity is a private retirement account (INDIVIDUAL RETIREMENT ACCOUNT), until you withdraw the revenues.

Deferred and prompt annuities supply numerous options you can select from. The choices offer different levels of potential threat and return: are ensured to earn a minimal rates of interest. They are the most affordable monetary risk however give lower returns. earn a greater rates of interest, yet there isn't an ensured minimum rate of interest price.

Variable annuities are greater risk because there's a chance you could shed some or all of your money. Set annuities aren't as dangerous as variable annuities because the financial investment risk is with the insurance firm, not you.

Highlighting Fixed Vs Variable Annuities A Closer Look at Fixed Annuity Or Variable Annuity What Is the Best Retirement Option? Pros and Cons of Various Financial Options Why Choosing the Right Financial Strategy Matters for Retirement Planning Variable Annuities Vs Fixed Annuities: How It Works Key Differences Between Different Financial Strategies Understanding the Risks of Variable Annuity Vs Fixed Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing Fixed Vs Variable Annuity FAQs About Fixed Indexed Annuity Vs Market-variable Annuity Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Fixed Vs Variable Annuities A Beginner’s Guide to Fixed Index Annuity Vs Variable Annuity A Closer Look at How to Build a Retirement Plan

If efficiency is low, the insurance provider bears the loss. Fixed annuities ensure a minimum passion rate, normally in between 1% and 3%. The firm could pay a higher rates of interest than the assured rates of interest. The insurance provider identifies the rates of interest, which can change regular monthly, quarterly, semiannually, or each year.

Index-linked annuities reveal gains or losses based on returns in indexes. Index-linked annuities are extra complicated than repaired delayed annuities. It is essential that you recognize the functions of the annuity you're thinking about and what they suggest. The 2 contractual functions that affect the amount of rate of interest credited to an index-linked annuity one of the most are the indexing method and the engagement price.

Understanding Annuity Fixed Vs Variable A Closer Look at How Retirement Planning Works What Is the Best Retirement Option? Pros and Cons of Fixed Vs Variable Annuity Pros And Cons Why Choosing the Right Financial Strategy Is Worth Considering Fixed Vs Variable Annuities: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Risks of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Tax Benefits Of Fixed Vs Variable Annuities Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Tax Benefits Of Fixed Vs Variable Annuities A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

Each counts on the index term, which is when the company determines the rate of interest and credit reports it to your annuity. The establishes just how much of the boost in the index will certainly be made use of to determine the index-linked rate of interest. Various other crucial attributes of indexed annuities consist of: Some annuities top the index-linked rate of interest.

Not all annuities have a floor. All dealt with annuities have a minimal guaranteed worth.

Understanding Annuities Fixed Vs Variable Key Insights on Annuity Fixed Vs Variable Defining the Right Financial Strategy Benefits of Choosing the Right Financial Plan Why Choosing the Right Financial Strategy Is a Smart Choice Pros And Cons Of Fixed Annuity And Variable Annuity: How It Works Key Differences Between Retirement Income Fixed Vs Variable Annuity Understanding the Rewards of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Fixed Income Annuity Vs Variable Growth Annuity A Beginner’s Guide to Variable Annuities Vs Fixed Annuities A Closer Look at Variable Vs Fixed Annuity

Various other annuities pay compound passion throughout a term. Compound passion is interest earned on the cash you saved and the passion you make.

If you take out all your money prior to the end of the term, some annuities won't attribute the index-linked rate of interest. Some annuities might credit only part of the passion.

This is due to the fact that you birth the investment risk instead of the insurer. Your agent or economic consultant can help you decide whether a variable annuity is appropriate for you. The Stocks and Exchange Commission classifies variable annuities as safety and securities due to the fact that the performance is stemmed from supplies, bonds, and various other financial investments.

An annuity agreement has two phases: a buildup stage and a payment stage. You have a number of options on just how you contribute to an annuity, depending on the annuity you get: enable you to choose the time and amount of the settlement.

The Internal Earnings Solution (INTERNAL REVENUE SERVICE) controls the taxes of annuities. If you withdraw your earnings before age 59, you will probably have to pay a 10% very early withdrawal fine in enhancement to the tax obligations you owe on the interest made.

After the buildup stage finishes, an annuity enters its payout stage. There are numerous options for obtaining payments from your annuity: Your firm pays you a dealt with amount for the time mentioned in the contract.

Decoding How Investment Plans Work A Comprehensive Guide to Investment Choices Breaking Down the Basics of Immediate Fixed Annuity Vs Variable Annuity Advantages and Disadvantages of Variable Vs Fixed Annuities Why Choosing the Right Financial Strategy Is a Smart Choice How to Compare Different Investment Plans: Explained in Detail Key Differences Between Immediate Fixed Annuity Vs Variable Annuity Understanding the Rewards of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing Variable Vs Fixed Annuities FAQs About Fixed Interest Annuity Vs Variable Investment Annuity Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Deferred Annuity Vs Variable Annuity A Closer Look at How to Build a Retirement Plan

Many annuities bill a fine if you take out money prior to the payout phase. This fine, called an abandonment charge, is typically greatest in the early years of the annuity. The charge is frequently a portion of the taken out money, and normally begins at about 10% and drops yearly until the abandonment duration mores than.

Annuities have actually other fees called lots or payments. In some cases, these fees can be as much as 2% of an annuity's value.

Variable annuities have the possibility for greater incomes, but there's more threat that you'll shed cash. Be careful concerning placing all your properties right into an annuity. Representatives and business need to have a Texas insurance coverage license to legitimately offer annuities in the state. The issue index is an indication of a company's customer care record.

Annuities sold in Texas has to have a 20-day free-look duration. Replacement annuities have a 30-day free-look duration.

{kind=link}

Table of Contents

Latest Posts

Exploring the Basics of Retirement Options Key Insights on Your Financial Future What Is Fixed Vs Variable Annuity Pros And Cons? Benefits of Annuities Fixed Vs Variable Why Choosing the Right Financi

Decoding How Investment Plans Work Key Insights on Fixed Annuity Or Variable Annuity Defining Fixed Income Annuity Vs Variable Growth Annuity Advantages and Disadvantages of Annuities Variable Vs Fixe

Breaking Down Pros And Cons Of Fixed Annuity And Variable Annuity A Comprehensive Guide to Fixed Vs Variable Annuities Breaking Down the Basics of Deferred Annuity Vs Variable Annuity Pros and Cons of

More

Latest Posts